Get In Touch

- Direct Message: 417-714-0501

- Office Phone: 417-218-0088

- Email: admin@theinsuranceeducators.com

-

Office: 730 W Center Circle

Nixa, MO 65714

Medicare Supplements

Simplifying Insurance for Individuals, Families, Business Owners, & their Loved Ones across the US

Original Medicare covers many healthcare services, but it doesn’t cover everything. To help cover costs that Original Medicare doesn’t, such as copayments, coinsurance, and deductibles, you can purchase a Medigap policy from a private insurance company. Some Medigap plans also offer additional coverage for services not included in Original Medicare, like medical care while traveling abroad.

When you have Original Medicare and a Medigap policy, Medicare pays its share of the Medicare-approved amount for covered healthcare costs first. Then, your Medigap policy covers its portion. Note that Medicare does not contribute to the cost of Medigap premiums.

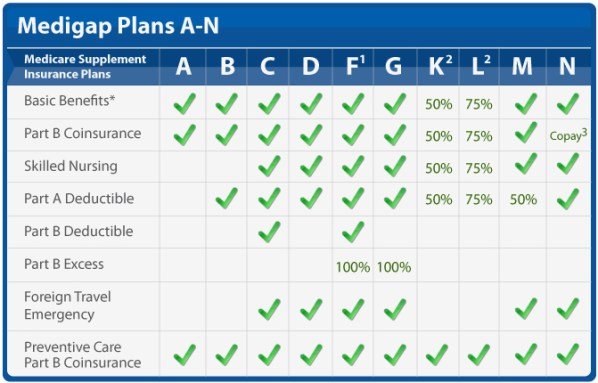

Medigap policies must adhere to federal and state regulations designed to protect you and must be clearly labeled as “Medicare Supplement Insurance.” These policies are standardized and identified by letters in most states, with each plan offering the same basic benefits but varying in additional coverage options.

*Note: In Massachusetts, Minnesota, and Wisconsin, Medigap policies are standardized differently.

While the costs for each Medigap plan will differ among insurance companies, the coverage of each plan will remain the same.

When shopping for a Medigap policy, ensure you are comparing identical plans across different insurance companies. For example, compare Plan A from one company with Plan A from another, as the benefits for each plan type are standardized.

In certain states, you may come across Medicare SELECT policies. These Medigap policies require you to use specific hospitals and sometimes specific doctors to receive full coverage. However, if you purchase a Medicare SELECT policy, you have the right to switch to a standard Medigap policy within 12 months if you decide it’s not the right fit for you.

More About Medigap Policies

Medigap Carriers

Here’s what you need to know about Medigap policies:

- Eligibility: You must have both Medicare Part A and Part B to purchase a Medigap policy.

- Premiums: You’ll pay a monthly premium for your Medigap policy on top of your monthly Part B premium.

- Coverage: Each Medigap policy covers only one person. If you and your spouse both want coverage, you each need to purchase separate policies.

- Best Enrollment Period: The optimal time to buy a Medigap policy is during the 6-month period that starts on the first day of the month you turn 65 and are enrolled in Part B. In some states, there are additional open enrollment periods. For instance, if you turn 65 and enroll in Part B in June, the best time to purchase a Medigap policy would be from June to November.

- Cost Variations: Medigap policy costs can vary and may increase as you age. It’s important to compare policies and check if your state has any cost limitations.

- Under 65: If you’re under 65, you won’t have the open enrollment period until you turn 65, though some states might offer options to buy a policy before then.

- Switching Plans: If you have a Medigap policy and decide to join a Medicare Advantage Plan (such as an HMO or PPO), you might want to cancel your Medigap policy as it won’t cover any expenses under your Medicare Advantage Plan. Contact your insurance company to cancel your Medigap policy. Note that once you drop it, you might not be able to get it back if you switch back to Original Medicare.

- Legal Protections: If you’re enrolled in a Medicare Advantage Plan, it’s illegal for anyone to sell you a Medigap policy unless you’re switching back to Original Medicare. If someone attempts to sell you a Medigap policy under these circumstances, contact your State Insurance Department for assistance.

Information provided by: Medicare and You Handbook 2025

Frequently Asked Questions

What is Medicare and who can get it?

Medicare is primarily used by individuals aged 65 and older, though some younger people may also qualify, including those with disabilities, permanent kidney failure, or amyotrophic lateral sclerosis (Lou Gehrig’s disease). While Medicare helps cover various healthcare costs, it does not fully cover all medical expenses or most long-term care costs.

Can I change my Medicare coverage?

Yes, you can adjust your Medicare coverage during specific enrollment periods, including the Annual Enrollment Period (AEP) and the Medicare Advantage Open Enrollment Period (MA OEP). Outside of these times, you may qualify for a Special Enrollment Period (SEP) if you experience certain life events, such as moving, losing other coverage, or becoming eligible for Medicaid.

What are the different parts of Medicare?

Medicare is divided into four parts:

- Part A: Hospital Insurance

- Part B: Medical Insurance

- Part C: Medicare Advantage Plans

- Part D: Prescription Drug Coverage

Where can I get more information about Medicare?

For more information about Medicare, you can visit the official website at www.medicare.gov, contact the Medicare hotline at 1-800-MEDICARE (1-800-633-4227).

We’re here to help you explore the options that best fit your needs. Contact us today for a free consultation, and let us guide you through your choices. Call us at 417-218-0088 or click “Call Now” below to get started!